In recent years, when handling divorce dispute cases, our matrimonial and family law team has encountered an increasing number of issues concerning the division of insurance assets in the partition of marital joint property. For instance, a recent case we handled involved the disposal of insurance products.

Ms. Zhang and Mr. Wang agreed to a consensual divorce due to marital estrangement. The two initially reached an agreement on the division of real estate, vehicles, bank deposits and company equity within their marital property. However, they held divergent views and failed to reach a consensus when it came to the division of insurance products.

The parties purchased an annuity insurance policy, with Mr. Wang as the policyholder and Ms. Zhang as the insured. The premium payment term was set at ten years, with an annual premium of RMB 200,000. By the time the dispute arose, seven years of premiums had been paid, with three years still outstanding. The current cash value of the policy stands at RMB 1.2 million.

During negotiations, Ms. Zhang claimed that the division should be based on the total payable premium of RMB 2 million, and demanded that Mr. Wang compensate her RMB 1 million.

Mr. Wang argued that Ms. Zhang’s claim was unreasonable and unacceptable. He proposed changing the policyholder to Ms. Zhang, with Ms. Zhang undertaking the remaining premium payments herself. Meanwhile, Ms. Zhang should compensate him half of the premiums already paid, namely RMB 700,000.

Who has a reasonable claim, Ms. Zhang or Mr. Wang?

How should insurance policies purchased during marriage be divided?

From the perspective of insurance nature, insurance can be divided into social insurance and commercial insurance. In terms of insurance subject matter, insurance is classified into personal insurance and property insurance, among which personal insurance is most closely related to daily life. The following discussion focuses mainly on personal insurance products within commercial insurance.

Whose Insurance Policies Are Subject to Division?

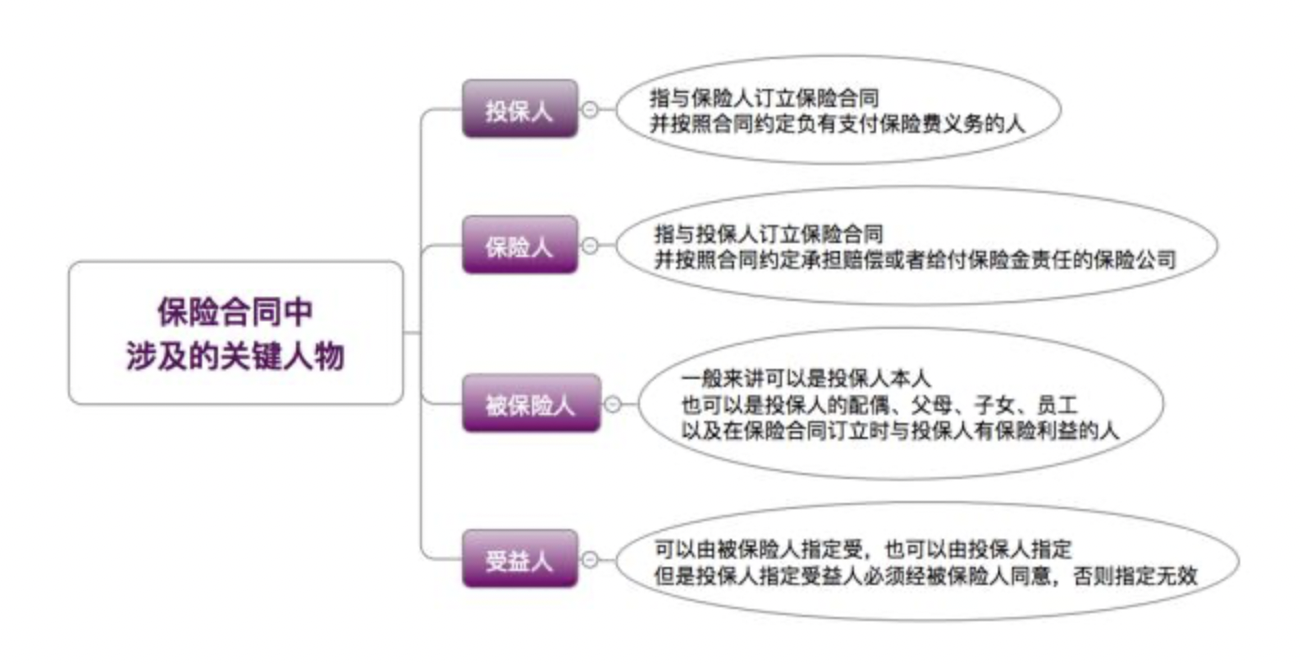

An insurance contract involves three parties: the policyholder, the insurer, and the insured.

On the basis of clarifying all parties to an insurance contract, it shall be made clear that: the cash value of an insurance policy belongs to the policyholder. Only where either spouse acts as the policyholder and owns the policy cash value may such insurance policy be regarded as marital joint property and subject to division upon divorce.

Which Insurance Products Are Divisible?

Personal insurance is categorized into life insurance, health insurance, annuity insurance and accident insurance.

Products such as life insurance, annuity insurance, and critical illness insurance under health insurance are divisible because they carry cash value.

Property insurance, as well as accident insurance and medical insurance within personal insurance, belong to expense-type insurance. Their value is basically consumed on an annual basis with little or no cash value, and thus will not be discussed herein.

Under What Circumstances May Insurance Policies Be Divided?

The prerequisite for dividing insurance products upon divorce is that no insured event has occurred and no insurance compensation has been received.

If an insured event has already taken place, the insurance compensation obtained under health insurance contracts and accident insurance contracts, as well as the insurance compensation acquired by either spouse as a beneficiary under life insurance contracts with death as the payment condition, shall, under current judicial practice, be recognized as the personal property of the respective spouse and generally not be subject to division.

To sum up, how exactly do courts in judicial practice divide insurance products purchased during the subsistence of marital relationship?

There are no explicit provisions stipulated by law on this matter. We hereby summarize and share the courts’ adjudication approaches in judicial practice. Generally speaking, when dividing insurance products, courts mainly make rulings according to differences in insurance structure:

-

The policyholder and the insured are the same spouse The arrangement shall be subject to the will of the policyholder, who may either surrender the policy or continue to hold it. In either case, the policyholder shall compensate the other spouse with half of the policy’s cash value.

-

One spouse as the policyholder, and the other spouse as the insured In this scenario, the parties may reach an agreement through negotiation. Alternatively, the policyholder may surrender the policy, and both parties divide the policy cash value. If the insured refuses to surrender the policy, the insured may continue to hold the policy, compensate the other spouse with half of the cash value, and apply for a change of policyholder.

-

One spouse as the policyholder, and their child as the insured In judicial practice, the insurance interest under such a policy is deemed a gift made by both spouses to their child, and is generally not subject to division. After divorce, if the party who obtains custody of the child is not the existing policyholder, such party may apply to change the policyholder so as to continue holding the policy.

With the above analysis, the method for dividing the insurance product in the earlier case involving Ms. Zhang and Mr. Wang becomes very clear:

First, the insurance product was purchased with marital joint property during the marriage, and shall therefore be deemed marital joint property.

Second, the divisible property value shall be calculated based on the current policy cash value of RMB 1.2 million, rather than the paid-in premium of RMB 1.4 million, still less the total payable premium of RMB 2 million.

Finally, the specific division plan shall be determined according to whether the policyholder surrenders the policy or retains it:

-

If Mr. Wang surrenders the policy, both parties shall equally divide the surrender proceeds obtained from the insurance company, namely the cash value of RMB 1.2 million, with each party entitled to RMB 600,000.

-

If Mr. Wang intends to surrender the policy while the insured Ms. Zhang wishes to keep it, Ms. Zhang may negotiate with Mr. Wang to compensate him half of the policy cash value, i.e., RMB 600,000, and apply to change the policyholder from Mr. Wang to herself so as to continue holding the policy.

To sum up, the above illustrates the practical application of how insurance, as a special type of marital joint property, shall be divided upon divorce.